There is a constant flux of carbon market size calculations and projections. This gets a lot of attention in the voluntary carbon markets, currently valued at around $2 billion and growing. Every now and then, the size of compliance carbon markets, valued over $800 billion, also features in the limelight. Estimates for international Article 6 carbon market size today are harder to come by, but it is expected to be at $1 trillion in 2050.

Below, I explore why making such estimations is increasingly inconsistent and incomparable. Preparing meaningful data to inform decision-making requires new carbon market qualifiers that can be tracked, compared, and relied upon.

There are two areas this blog post does not venture into – authorisation under Paris Agreement Article 6 and Nationally Determined Contribution (NDC) conditionality – these topics deserve a separate piece to do them justice.

How are compliance markets defined?

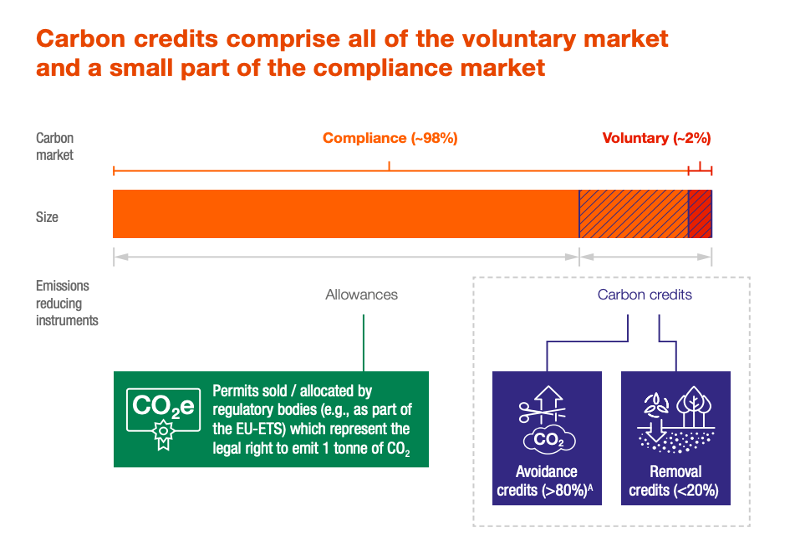

There is no commonly agreed definition. Compliance markets are often limited to emissions trading systems (cap-and-trade systems) (1, 2, 3). Other times, carbon crediting markets like the offsetting scheme for international aviation (CORSIA), Kyoto Protocol compliance markets and Article 6 under the Paris Agreement as international compliance markets are also considered. When trying to quantify market developments, the definition and its scope matter.

Given that carbon allowances in emission trading systems and carbon credits in carbon crediting mechanisms are incomparable, does it even make sense to calculate the market size by combining both cap-and-trade and carbon crediting compliance markets?

Are Article 6 markets compliance markets?

I asked this question in a LinkedIn post a while ago and received a treasure trove of comments from some of the best minds in the field. That thread inspired this blog post.

The Kyoto Protocol had compliance markets designed for countries to meet their climate targets. When compliance demand disappeared, the Clean Development Mechanism started supplying the voluntary markets. Under the Paris Agreement, countries can decide whether and how they use Article 6 markets. For a regulatory regime, for other (for example, voluntary) purposes, or for both? So, while Article 6 might be predominantly used for compliance, that is not the only use.

There are multiple threads in the relationship between Article 6 and voluntary markets. When the Paris Agreement was negotiated, the voluntary market participants informed the wording of Article 6. Today, there are already examples of Article 6 being used to cater to voluntary market demand. For example, Switzerland uses Article 6 credits in its domestic voluntary carbon market (see the objective section in bilateral agreements). Countries like Sweden are using voluntary market infrastructure for bilateral carbon credit deals. Next to that, the voluntary market standards inform the design of Article 6.4 Mechanism and simultaneously build Article 6 relevance into its standards.

Considering the above, it’s unsurprising that some experts see Article 6 markets as hybrid or integrated markets.

Carbon markets are converging in multiple ways

It’s not only Article 6 where the lines between compliance and voluntary supply and demand are blurring. It also happens to some extent with different emissions trading systems used for voluntary offsetting. In France, the label bas-carbone is an example of a government-led supply that can only be used for voluntary purposes.

California’s emissions trading system and CORSIA allow certain voluntary market credits for compliance. The same goes for carbon taxes established in Colombia and South Africa.

The EU’s Carbon Removal Certification Framework is currently being designed with the voluntary market as one of the use cases. Still, the mid-term expectation is that at least some removal credits will find their way into compliance use. The CCS+ initiative is built for the voluntary market standard but is designed with both voluntary and compliance use in mind.

The convergence of compliance and voluntary markets will never be complete. Jurisdictions like the US are unlikely to establish carbon markets on a federal level. And voluntary markets will continue to do what they do best – being a testing and piloting ground for new solutions and technologies that are not yet under the regulatory regime and contributing to the improvement of compliance markets through this experience.

So, how to slice the carbon markets?

The dichotomy of compliance and voluntary markets is becoming unhelpful. First, there’s a lack of agreement on what compliance markets are, especially concerning carbon crediting markets. And second, the consistent convergence of the two makes it increasingly difficult to distinguish them. Will the markets move on to establish new qualifiers, and will market actors embrace these?

This situation reminds me of the carbon removal vocabulary discussions where most stakeholders agree that dividing removals between technological and nature-based is unhelpful for various reasons but struggle to come up with easy-to-communicate alternatives. Hence, these terms live on and are still sometimes used when quantifying the carbon removal market segments, although there is progress.

Keeping emissions trading systems and carbon crediting mechanisms separate seems practical due to their differing nature. Next to that, there is an obvious need to divide the market into supply and demand sections. On the supply side, there is the voluntary supply from independent standards and compliance supply from emissions trading systems and the Article 6 markets. And on the demand side, the voluntary demand by the corporates and compliance demand by emissions trading system participants and governments for achieving their NDCs.

Demand and supply

The convergence of compliance and voluntary markets creates new challenges and opportunities. The convergence of the market is an ample opportunity for voluntary supply that can tap into both voluntary and compliance demand. However, corporate buyers will compete with governments for the same credits so that the demand might outstrip supply.

Parallel concerns around the fundamental supply and demand imbalance are rising regarding CORSIA. Developers, analysts, and airlines have highlighted a potential shortage of carbon credit supply later in the decade.

A single-level playing field for compliance and voluntary market buyers has some advantages, including increased demand for carbon credits, more efficient markets, simplified regulation, and improved environmental integrity. However, it may also lead to higher costs for compliance buyers and reduced access for voluntary market buyers, potentially increasing market complexity.

Article 6 markets will not only converge but also directly compete with voluntary markets. Countries relying on Article 6 markets to meet their NDCs may find the cheapest source of carbon abatement already captured by the voluntary markets, leaving expensive abatement opportunities for the purchasing countries. Voluntary markets have the head start here, considering how lengthy the process of setting up the Article 6 rulebook has been.

Following the developments in demand and supply offers better insights than only tracking market size. This will also tackle the current confusion where some estimations expect voluntary markets to keep growing mid-to-long term, and others expect a contraction in the long term due to expanding compliance markets.

Final words

Having meaningful carbon market data to inform decision-making requires new carbon market qualifiers that can be tracked, compared, and relied upon. As different market segments keep getting more intertwined, there is no perfect way to divide the carbon markets. The division of compliance versus voluntary carbon markets only works for a very generalist audience. Going forward, keeping emissions trading systems and carbon crediting mechanisms separate is a good start. The first entails a compliance market, and the second includes both compliance and voluntary markets. Given the potential imbalances of voluntary and compliance supply and demand, it is worth quantifying compliance demand, compliance supply, voluntary demand and voluntary supply separately.

***

Thank you for reading! Sign up for updates below, and stay tuned for the next posts.

Would you like to use (parts of) the text? Go ahead on the condition that you explicitly refer to this post and include a link.

Thank you!