This blog post has been co-authored with Asger Strange Olesen, Member of the EU Carbon Removal Expert Group and AFOLU Policy aficionado since 2009.

The latest farmer protests in numerous European capitals, the (hopefully soon) adopted Nature Restoration Law, and the need to scale up carbon removal to meet climate targets have all contributed to bringing the land sector to the forefront of discussions.

However, the land sector has not featured prominently in the EU’s 2040 climate target debate so far. A quantified contribution of the agriculture sector was featured in the leaked version of the EU’s vision for its 2040 Climate Target, only to be scrapped from the final version.

Land sector – farms, forests and wetlands

Separating the “land sector” from other sectors in the EU climate architecture has featured in discussions since 2015 but has not been formalised. It combines activities reported under the Agriculture and Land Use, Land Use Change and Forestry (LULUCF) sectors of the IPCC Guidelines for national greenhouse gas inventories, sometimes referred to in combination as AFOLU. Essentially, the land sector consists of farms, forests, and wetlands.

Potential for removals

The land sector today features significant biogenic emissions from husbandry, fertiliser use, and drainage of peatlands. At the same time, in several EU countries, the LULUCF part of the sector contributes a net sink, albeit a declining one. Recent European Commission projections show that the current all-time-low net sink of -230 Mt/yr (2021) will remain much short of the -310 target by 2030 unless incentives in the order of 50 Euro/ton are introduced. The EEA is projecting a 50Mt shortfall in 2030. The current declining trajectory of the land sector sink would lead to missing the necessary appx -410 Mt of removals in 2050 to reach the climate law’s neutrality target.

Even with a projected increase in technological removals available at acceptable market prices in 2050, more land removals are needed to offset residual emissions from all emitting sectors: currently around 100 Mt more. Meanwhile, the potential of increasing removals from the land sector is there but needs thoughtful policy design to bring about.

How to get there?

The EU’s Carbon Removal Certification Framework (CRC-F) is the first try to establish business models to scale removals, including from the land sector. The recently agreed regulation still leaves many questions unanswered:

–> Where will the demand come from (who will pay)?

–> What are the different use cases?

–> How will the Carbon Removal Certificates (CRCs) be “nested” in national inventories?

–> How will we govern CRC flexibility between sectors and member states, if at all?

Clear incentives on the land manager level, combined with substantial private funding, are needed for the land sector to meet the -310 Mt/yr carbon removal target by 2030 and, by 2050, altogether 100 Mt more annual carbon removal across the EU.

Tackling this via a harmonised EU framework makes the most sense, given how challenging it would be to build well-funded and stable incentive systems separately from the ground up in all 27 EU Member States. Also, land use intensity varies significantly within and between the MS, as do carbon removal potential and existing carbon stocks, warranting an approach to incentivise and govern cost-effective distribution of action between MS and avoid protective MS siloing.

This post explores how to build a framework that can mobilise the needed level of investments by using the 2040 climate target architecture, CRCs, and improved nesting of land sector accounting between the two.

Building on the existing climate target architecture

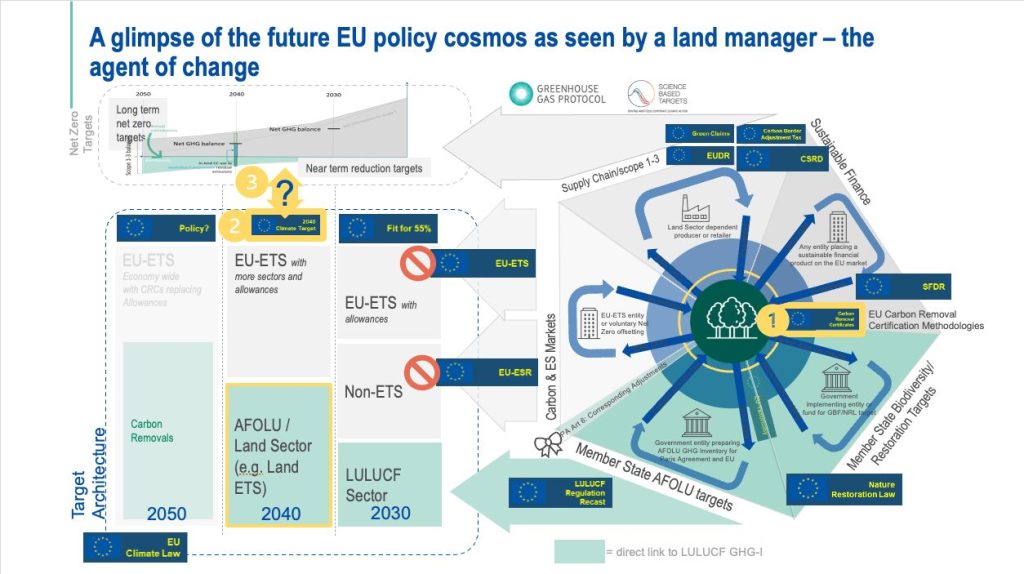

The European Commission’s vision for the EU’s 2040 climate target was published in February 2024 and is outlined in more detail in the previous blog post. The legislative proposal offering more details on the target’s architecture is expected in 2025. This means at least one more year of lack of policy certainty, especially for scaling up removals.

As the current architecture stands, the EU ETS has an EU-wide target, whilst the Effort Sharing Regulation (ESR, largely non-CO2 agriculture, waste, transport, and buildings1) and LULUCF have country-specific targets.

Assuming that the same fundamental target architecture remains in place for the 2040 target or an early version of a Land Sector ETS is tested, here is a package of four unconventional policy design ideas to provide clarity and create demand for CRCs to incentivise carbon removal from the land sector. These features are mutually dependent and can serve as an inspiration for policymakers when considering the target design.

Design feature 1 – “Like for like” for the land sector

This option requires establishing the long-debated land sector (which currently doesn’t formally exist) with a distinct net-zero target by 2040. Given that the Climate Law will be reopened to introduce the upcoming 2040 target, introducing such an EU-level sub-target for the land sector could be a way forward.

The CRC-F was proposed to be used for various types of results-based finance, not only carbon crediting. One of those other purposes could be using the framework to create a mandatory scheme for the land sector – a supply chain programme built on GHG inventory/footprint based 2030, 2040 and 2050 targets. Its goal: reporting emissions and removals consistently and credibly through the whole value chain, including finance for the same Land Manager activity.

To allow that, the methodologies developed under the CRC-F would need to be designed to work for two purposes: inventory/footprint and carbon crediting, with certain sections (including full additionality and permanence aspects) used only when certifying for carbon crediting.

The CRC-F certificate can reflect both results, particularly if the methodology and unit types are clearly separated based on the use cases. For carbon crediting, the units could be called Carbon Crediting Units, whilst, for the inventory/footprint-based approach, these could be called Reporting Units (Removal Reporting Units and Soil Carbon Reduction Units based on the current scope of the CRC-F). Reporting Units could also become the basis of the MRV under the new potential agriculture ETS.

From the policy design perspective, there will need to be a market infrastructure that enables implementing such an approach and rules governing it. While it is not proposed that MS have individual, negotiated Land Sector net-zero targets like in the ESR, rules for MS-level accounting and flexibilities of certified removals by ESR entities would be needed. More features of one such mechanism for this are the ones presented below.

Design feature 2 – Regulate target and actions for demand

This would be a complementing piece of regulation, installing a domestic mechanism building on the existing approach of the Regulation for Deforestation-free products (EUDR), Sustainable Finance Disclosures Regulation (SFDR) and Carbon Border Adjustment Mechanism (CBAM): by 2040, any non-SME actor within a sector of economic activities that places product on the EU market with an EU based land sector footprint must achieve the same net GHG target as the EU level target.

Direct transposition of e.g. a 90% EU net emission reduction target to actors while allowing the use of ‘reporting type’ CRCs as documentation for in-scope neutralisation2 would streamline and drive efforts to reach the 90% reduction by 2040. For a start, the mechanism should target large food producers, wooden furniture and construction materials manufacturers, and grocery retailers, among others. For companies that cannot reach their reduction target in scope, there should be access to a limited number of ‘crediting type’ CRCs.

The mechanism should apply minimum thresholds based on company size or turnover and perhaps land sector exposure (e.g. percentage emission in the land sector, similar to SBTi Forest, Land and Agriculture – FLAG). Starting out by targeting NACE categories with substantial land sector footprints would be a plausible way forward and complement the mentioned regulatory efforts to enhance the traceability of supply chains.

To ensure proper nesting in the GHG inventory of the operator’s host MS, the governments would need to establish guidelines ensuring that the net-removal activities covered by this mechanism would be nested in the national GHG inventory (see design feature 4 below), as registered reporting type CRCs, whereas ‘crediting type’ CRCs would need a clearing house mechanism is used cross-border within the Union.

Even if implemented as a one-year target for 2040, with no requirements before that year to allow the transformation to be prepared, this mechanism could bring us a long way towards land sector neutrality.

Design feature 3 – Combined ESR and Land Sector Net Zero at MS level

If there is support for maintaining a version of the current ESR sector for the 2040 climate target architecture, this would most likely be the home for many of the downstream companies serving as off-takers of output from farms and forests. The companies within the sectors with land-based supply chains (also within the scope of option 2 above) would be subject to MS-level policy initiatives to reach any negotiated MS level 2040 ESR target or ‘shared effort’. These companies would, therefore, also finance the land sector efforts to increase removals and, in return, be allowed to use ‘reporting type’ CRCs towards the entity-level net-reduction target imposed by option 2 above.

If ESR-sector companies with substantial land sector GHG footprint have mandatory 90% net reduction targets following from option 2 above, but at MS level, there is a net zero target for the combined LULUCF and ESR sectors by 2040, there is a gap. MS can choose to address this gap with national policies. Where the government is a major land manager of public lands, its own ‘scope 1’ action might be the way forward, or where agriculture is net positive, CAP interventions might be most suited.

Design feature 4 – Nesting

The CRC-F provisional agreement demands consistency with the EU NDC. But over time, we must go further. First, a simple workable definition of the term ‘nesting’ applied here is: ensuring that private emission reductions and removals are fully reflected in a national GHG inventory. Simplified, private and public/national GHG inventories alike consist of two steps that feed a third: estimation, reporting, and then accounting towards a target. Sometimes there’s measurement before estimation, but it is rare and can be considered part of estimation.

Mindful of these three steps, nesting can happen at three levels:

1) Ensuring the estimation for each plot, parcel, or property within a country always uses the same methods and input data, no matter the owner or the use. That way, there is one joint inventory that feeds both private and public reporting and accounting needs. Beautiful as a concept, difficult in practice. It includes consistent representation of land in a spatially explicit manner and maintaining mass balance for all lands, as well as the use of the same emission factors (if using the Tier 2 method from the IPCC Guidelines).

2) Ensuring aligned estimation methods produce comparable data that must feature in separate columns in the national reporting. Simple plug-in in principle, but it would be almost impossible to avoid property overlaps, gaps, and inconsistencies without having level 1 above in order.

3) Ensuring national accounting targets recognise private targets and emission reduction and removal contributions and that CRC units issued for corporate use are reconciled in the government accounting (if not already nested at level 1 or 2). Sounds simple but almost impossible due to property overlaps, gaps, and inconsistencies. And a very political space with a poor track record for clarity.

The first option would be ideal and shows how a nested private reporting system should function when national GHG inventories are ready to host them. Achieving that will take 5-10 years, investments, and a re-thinking and work scope increase of national inventories by governments and inventory teams.

To get this process moving, the EU2040 target framework should include a time-sequenced or stepwise introduction of requirements to drive us through the three levels and thus revolutionising the existing practice by:

–> Recognising all private sector units issued and corresponding corporate claims as memo items in separate columns in the EU GHG accounting, effectively separating where private initiative or government schemes or regulations drove reductions or removals over the past year.

–> Reporting all land manager scope 1 reporting next to LULUCF inventory numbers in separate columns from 2030 until 2040, with full, nested, and mandatory reporting thereafter.

–> Producing MS level user guide – or simply Good Practice Guidelines – for estimation of corporate GHG budgets within national scope 1 land sector inventories that build on and ensure consistency with existing LULUCF inventory practices in each Member State. Setting out a stepwise learning curve towards mandatory Tier 3 estimation from 2040 and supporting adoption by land managers within the EU. The CRC-F methodologies and the EU taxonomy are solid starting points for the guidelines.

Conclusion

Using the 2040 climate target architecture, CRC-F, and improved nesting of land sector accounting between the two can mobilise the needed level of investments for the land sector. However, all four suggested policy design features have challenges regarding likely political support and implementation.

Building on the existing EU climate target infrastructure means that these features are more likely to facilitate the scale-up of removals than alternatives that require more elaborate changes to the current frameworks.

Given the climate neutrality target on the horizon, the status quo will not be able to deliver the scale of removals the EU needs. Hence, while there are no simple solutions, new design features must be introduced into the current policy framework to make progress.

Several ideas proposed in this blog post would benefit from further detailed exploration. We will cover that in future posts. Stay tuned!

Footnotes:

- Several ESR sectors (transport, buildings) belong to ETS II ↩︎

- Measures that companies take to counterbalance the climate impact of unabatable (i.e., residual) GHG emissions which are released into the atmosphere at and after net-zero target date through permanent removal and storage of CO2 from the atmosphere (SBTI) ↩︎

***

Thank you for reading! Sign up for updates below, and stay tuned for the next posts.

Would you like to use (parts of) the text? Go ahead on the condition that you explicitly refer to this post and include a link.

Thank you!